Most homeowners assume their homeowners insurance covers everything. Then the HVAC stops working on a July afternoon, and they get the news: that breakdown is not covered. A home warranty is the product designed to fill exactly that gap, yet most people buying or selling a home have only a fuzzy sense of what it actually does. This article breaks down the home warranty definition, explains the types of home warranties available, walks through real costs, and gives you an honest take on whether it is worth your money.

Table of Contents

- Key takeaways

- What is a home warranty, exactly

- Types of home warranties and what they cover

- Home warranty vs homeowners insurance

- Is a home warranty worth it for your home

- What homeowners get wrong about home warranties

- My take on home warranties after years of watching homeowners use them

- Protect your home beyond the warranty

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Home warranty vs insurance | A home warranty covers wear-and-tear breakdowns; homeowners insurance covers sudden damage from disasters or accidents. |

| What it covers | Most plans cover major systems like HVAC, plumbing, and electrical, plus built-in appliances. |

| How you pay | You pay an annual or monthly fee plus a service call fee each time a technician visits. |

| Is it worth it? | Value depends on your home’s age, appliance condition, and how often you expect to file claims. |

| Read the fine print | Coverage limits, exclusions, and service fees vary widely. Reviewing contracts carefully prevents surprises. |

What is a home warranty, exactly

A home warranty is a service contract between you and a warranty company. When a covered system or appliance breaks down due to normal use and age, you call the company, pay a service fee, and a contractor comes out to diagnose and fix the problem. The warranty company pays the repair or replacement cost up to the contract limits. That is it. No storm damage, no flooding, no theft. Just the predictable wear that happens to every home over time.

Home warranties cover the diagnosis, repair, or replacement of major components due to normal use, which makes them fundamentally different from homeowners insurance. Think of it this way: your insurance company cares about what happened to your home. Your warranty company cares about how long your appliances have been running.

The payment structure works in two layers. First, you pay an annual or monthly premium to keep the contract active. Second, every time you request a repair, you pay a service call fee per visit. That fee applies even if the technician determines the problem is not covered. Knowing this upfront changes how you think about when to file a claim.

Pro Tip: Before signing any contract, ask what the service call fee is and whether it changes based on the type of repair. Some providers charge different rates for appliance calls versus HVAC calls.

- Coverage kicks in after a waiting period, usually 30 days from contract start

- The warranty company selects the contractor, not you

- Coverage has per-item and annual caps that limit total payout

- Pre-existing conditions are generally excluded from coverage

Types of home warranties and what they cover

Not every plan is built the same. The three most common plan types give you a starting point for comparison.

| Plan Type | What It Covers | Best For |

|---|---|---|

| Systems only | HVAC, plumbing, electrical, water heater | Homes with new appliances but aging infrastructure |

| Appliances only | Dishwasher, oven, washer, dryer, refrigerator | Homes with older built-in appliances |

| Combination | Both systems and appliances | Most homeowners wanting broader protection |

Coverage typically includes major systems and built-in appliances, but the specifics vary significantly by provider and plan tier. A “systems plan” at one company might include the water heater while another lists it as an add-on. Always confirm what is in writing before assuming something is covered.

Common add-ons you can pay extra for include:

- Pool and spa equipment (pumps, heaters, filters)

- Roof leak repair

- Well pump coverage

- Septic system pumping

- Additional refrigerators or standalone freezers

Pool coverage deserves special attention. Pool plans cover mechanical equipment like pumps and filters, not structural components like liners or tiles. Many pool owners assume they are fully covered and get an unwelcome surprise when a liner cracks. That kind of nuance shows up across nearly every add-on category.

Home warranties also have clear exclusions. Windows and the physical structure of the home are commonly excluded, as are cosmetic issues and problems caused by improper installation or lack of maintenance.

Pro Tip: Ask the warranty company to send you the full sample contract before you pay anything. Read the exclusions section first. That section tells you more about the real value of a plan than the marketing summary ever will.

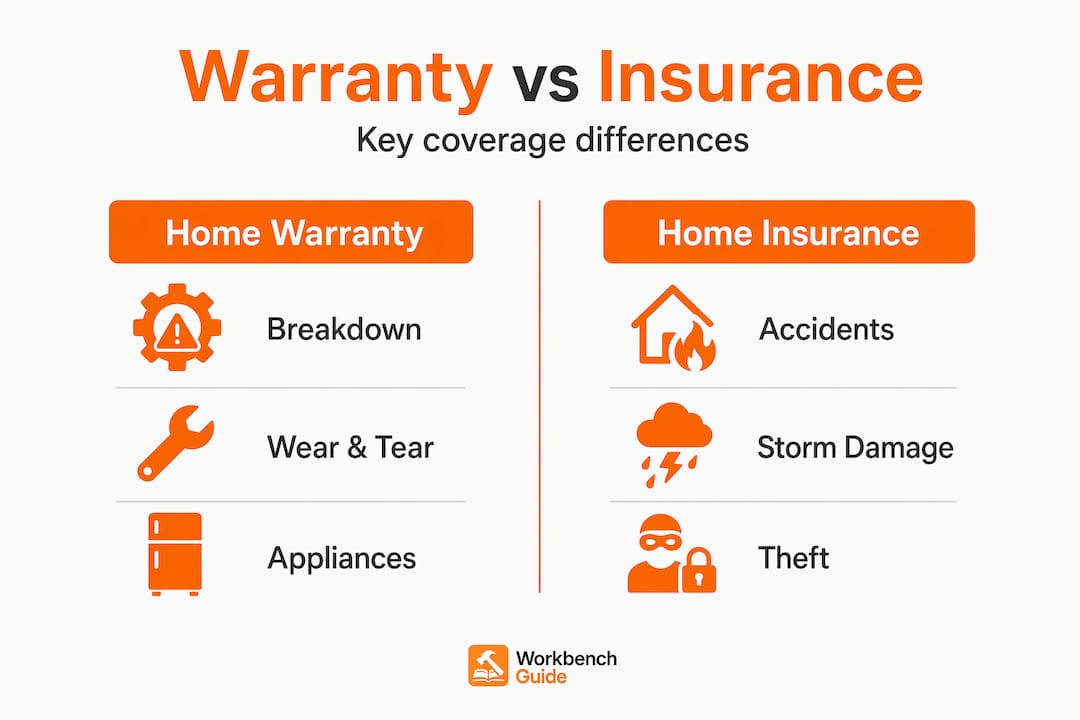

Home warranty vs homeowners insurance

These two products protect your home in completely different ways, and confusing them is one of the most expensive misunderstandings a homeowner can have.

Homeowners insurance exists to cover you against sudden, unexpected events: a fire, a burst pipe from a storm, a tree falling through your roof, or liability if someone is injured on your property. A home warranty covers wear-and-tear breakdowns not covered by insurance, meaning the refrigerator that quit after 12 years or the furnace that finally gave out.

Here is a side-by-side breakdown:

| Feature | Home Warranty | Homeowners Insurance |

|---|---|---|

| Trigger for coverage | Normal wear and tear | Sudden, accidental damage |

| What it protects | Systems and appliances | Structure, personal property, liability |

| Typical annual cost | $400–$1,000+ | $1,500–$2,000+ |

| Required by lenders | No | Yes (if you have a mortgage) |

| Contractor selection | Warranty company chooses | You choose (usually) |

You need both products for complete protection, but they serve different purposes. Your lender requires homeowners insurance. A home warranty is optional but can make financial sense depending on your home’s condition and age.

Is a home warranty worth it for your home

This is the real question, and the honest answer is: it depends. But you can make a smarter decision by running through a few specific factors.

-

Check your home’s age. Newer homes may have less need for a home warranty because builder warranties and manufacturer warranties on new appliances often cover early failures. A home built in the last three to five years with new appliances has much less to gain from a warranty in year one.

-

Add up the real costs. Pricing varies by state and plan tier. In Texas, for example, plans run roughly $45 to $85 per month, plus service fees of $75 to $150 per technician visit. If you file two claims in a year, your out-of-pocket cost could easily hit $800 before the warranty company pays a dollar toward parts.

-

Think about your appliances realistically. A 10-year-old HVAC system, an aging water heater, and a dishwasher on its last legs all represent real risk. A warranty starts looking attractive when you can identify multiple items that are likely to need service in the next few years.

-

Understand that a home warranty manages risk of service costs, not a guarantee of complete repairs. Coverage caps mean a company might pay $1,500 toward a $3,000 HVAC replacement. You cover the rest.

-

Research provider reputation. Read actual customer reviews, not just advertised claims. Look at how companies handle denied claims and how quickly contractors are dispatched.

-

Consider your comfort with DIY repairs. If you handle minor fixes yourself and know how to vet contractors, you might do better putting the annual premium into a dedicated home repair savings account.

The peak value scenario for a home warranty is an older home with aging systems, a buyer who prefers predictable expenses over surprise repair bills, and a plan with reasonable service fees and verified coverage for the specific items most likely to fail.

What homeowners get wrong about home warranties

The biggest source of frustration with home warranties is not the product itself. It is the gap between what people expect and what the contract actually delivers.

BBB complaints about warranties frequently stem from misunderstandings about coverage and claim processes. Warranty companies have flexibility in how they calculate payouts, and that flexibility rarely benefits the homeowner. Being aware of that going in changes how you shop.

A few things that trip people up repeatedly:

- Assuming all repairs are covered without reading the exclusions

- Not knowing the service fee applies even for denied claims

- Expecting coverage for items that were already malfunctioning at purchase

- Believing the warranty company will always approve the repair the technician recommends

“Plans vary significantly in coverage; buyers should confirm exactly what systems and appliances are covered rather than assume blanket protection.”

The best defense against disappointment is treating the contract like a legal document, not a marketing brochure. Reviewing contract terms thoroughly before signing and asking pointed questions about denial rates and coverage caps puts you in a much stronger position than most buyers.

My take on home warranties after years of watching homeowners use them

I have seen home warranties deliver real value and I have seen them leave homeowners frustrated, and the difference almost always comes down to one thing: expectations.

When a homeowner buys a warranty thinking it is a catch-all protection plan, they end up disappointed. When someone buys it specifically to manage the risk of a few aging systems, understands the service fee structure, and has read what is excluded, it often pays off. The product works best as a financial planning tool, not a safety net you never think about.

Where I think warranties fall short is when they become a substitute for actual home maintenance. A well-maintained HVAC lasts years longer than a neglected one, and no warranty covers damage from lack of upkeep. I have watched homeowners skip regular home inspections and routine servicing because they assumed the warranty had them covered. It does not work that way.

My honest advice: if your home is more than 10 years old and you have not replaced major systems or appliances recently, a combination plan is worth a serious look. But pair it with proactive maintenance. Know your appliances, schedule service on your HVAC annually, and use the warranty for what it actually is: a managed cost-sharing contract, not a replacement for caring for your home.

— Sean

Protect your home beyond the warranty

A home warranty handles breakdowns after they happen. Workbenchguide helps you prevent them in the first place. With smart maintenance reminders, step-by-step DIY guides, and project checklists built for homeowners, Workbenchguide keeps you ahead of the repairs that warranties often deny because of missed upkeep.

Start with the yearly maintenance checklist to build a simple routine that protects every major system in your home. If you want to go further, the preventative maintenance guide walks you through how to extend appliance lifespans and avoid the kind of wear that even a good warranty will not cover. When you know your home, you make smarter decisions about when a warranty is worth it and when your maintenance habits are doing the job already.

FAQ

What is a home warranty in simple terms?

A home warranty is a service contract that pays for the repair or replacement of major home systems and appliances when they break down due to normal wear and age. It is not insurance and does not cover damage from accidents or natural events.

What does a home warranty typically cover?

Most plans cover HVAC systems, plumbing, electrical systems, water heaters, and built-in kitchen appliances like dishwashers and ovens. Coverage specifics vary by provider and plan tier, so reviewing the contract is critical.

How is a home warranty different from homeowners insurance?

Homeowners insurance covers sudden damage from events like fires, storms, and theft. A home warranty covers mechanical breakdowns from everyday use and age, making the two products complementary rather than interchangeable.

How much does a home warranty cost?

Costs include an annual or monthly premium plus a service fee per technician visit. Depending on the state and plan, you might pay between $400 and $1,000 per year in premiums, plus $75 to $150 per service call.

Is a home warranty worth buying?

It depends on your home’s age and the condition of your systems and appliances. Older homes with aging HVAC, plumbing, or appliances often see real value from a combination plan, while newer homes with manufacturer warranties in place may see less benefit.